Commercial Real Estate in Central Oregon 2022

Commercial Real Estate in Central Oregon 2022

Main article written by broker Ron Ross, CCIM

January is a happy time for economic prognosticators. A fresh start and hearts full of optimism give rise to countless views on what the new year will bring. Here is mine.

Four major themes from 2021 will continue to drive Commercial Real Estate in Central Oregon in 2022: COVID, inflation, shortages, and slowing growth.

1. COVID

COVID is obviously first and foremost. The pandemic is evolving, unpredictable, and is not going away. Predicting the course of COVID has proven to be a fool’s errand. The best we can do here is look at how it has impacted our real estate market.

COVID has produced both winners and losers in the business and real estate worlds. Residential real estate markets in many locales, including Central Oregon, have exploded with in-migration. Increased working from home, the desire to escape high density, high traffic, and high crime urban areas, and the increasing importance of home as a place of refuge drive this trend. One only needs to spend a little time on the freeways of Southern California to appreciate the Central Oregon lifestyle, clean air and water, relatively easy commutes, access to recreation, and more. Let’s hope we can keep it.

As growth and demand for Central Oregon real estate signals a robust economy and builds wealth for homeowners and investors, the flip side is that it produces serious shortages and affordability problems.

The multifamily and industrial sectors have seen the same trends as residential housing. Low vacancies, rapidly rising rents, and a corresponding increase in market values reflect not only the residential in-migration but a growing trend of businesses moving in and starting up in Central Oregon. Industrial buildings are fully occupied and in huge demand. The increasing popularity of online commerce has created increased demand for storage and distribution. Multifamily and industrial are clearly winners in the COVID era. There will continue to be new supply of both product types built and brought to market.

Retail has been surprisingly resilient in the face of the pandemic. Many retailers were devastated. While some did not survive, many persevered with creative solutions, others thrived, and many are opening new businesses. It is a testament to the spirit of enterprise and optimism. Consumer demand is robust with record setting retail sales. Retail occupancy and lease rates are strong, and some new retail construction is either underway or in the pipeline.

The office sector is a different story. While the trend toward remote working is troubling for landlords, Bend office vacancies remain stable at under 10%. Lease rates are flat. The office is not going away anytime soon. Remote working presents plenty of challenges and inefficiencies, but the office market may be a net COVID loser in the long run and adjustments in that market are coming. There is no new office construction in Central Oregon.

2. INFLATION

Inflation is the next most dominant economic theme heading into 2022. A long history of super accommodative monetary policy from the fed, massive fiscal stimulus, a strong macroeconomic recovery, and supply and demand disruptions are the primary reasons for the most significant inflation in the last 35 years.

Real estate has long been known as a good inflation hedge. That is only partially true. The theory is that as inflation rises, rents will also rise. That does not hold true for properties that are locked into long term leases with low lease rate escalators. Like bonds, when inflation rises, the values for these properties can take a hit. Inflation also produces rising interest rates, and a corresponding increase in cap rates, again putting pressure on valuations.

Inflation is a mixed bag. It will be important for owners to ensure their income grows with the inflation rate.

3. SHORTAGES

Shortages will persist into 2022. Housing shortages, worker shortages, and product and service shortages that the developed world has long taken for granted will further fuel inflation pressures and will put some moderation to an otherwise booming economy and real estate market.

Central Oregon will feel these shortages as acutely as any region in the country. Housing affordability will continue to be problematic. Inconveniences and delays for all types of everyday goods and services will be commonplace.

4. SLOWING GROWTH

Slowing growth is relative. Reducing speed from 110 miles per hour to 80 is a slowdown. But 80 is still speeding (at least in Oregon). Slowing growth is still growth. No recession is on the horizon.

The hyper growth of 2021 is not sustainable, so a slowdown is inevitable. The Fed is changing course on monetary policy announcing the end to quantitative easing and probable interest rate hikes. For the most part that is good news, as it will help with inflation and supply chain disruptions.

Early 2022 indications are that the hot real estate market trends are still in full force. Central Oregon continues to be an attractive destination for in-migration and investment dollars.

Bend Office Market

Written by partner and broker Jay Lyons, SIOR, CCIM

Compass Commercial surveyed 223 office buildings totaling 2.76 million square feet for the fourth quarter office report of 2021. The market experienced 16,621 SF of absorption in the 4th quarter with a slight decline in vacancy rate from 7.12% to 6.52%. For the last six quarters, the office market has remained steady with the vacancy rate hovering between 6.50% and 7.50%. There is now 179,876 SF of office space available in the market.

LEASING: As evidenced by the slight decline in vacancy, the office leasing market is showing modest signs of improvement. The Downtown submarket improved the most with 13,022 SF of net positive absorption. The West Side submarket also experienced 3,790 SF of positive absorption, while the Highway 97/3rd Street submarket experienced 191 SF of net

negative absorption.

RENTS: Average asking rates on office space have remained steady and generally range between $1.70 and $2.15/SF/Mo. NNN with a handful of first-generation spaces exceeding this range. As is typically the case, the highest asking rates continue to be located within the West Side submarket with more affordable options available within the Highway 97/3rd Street submarket.

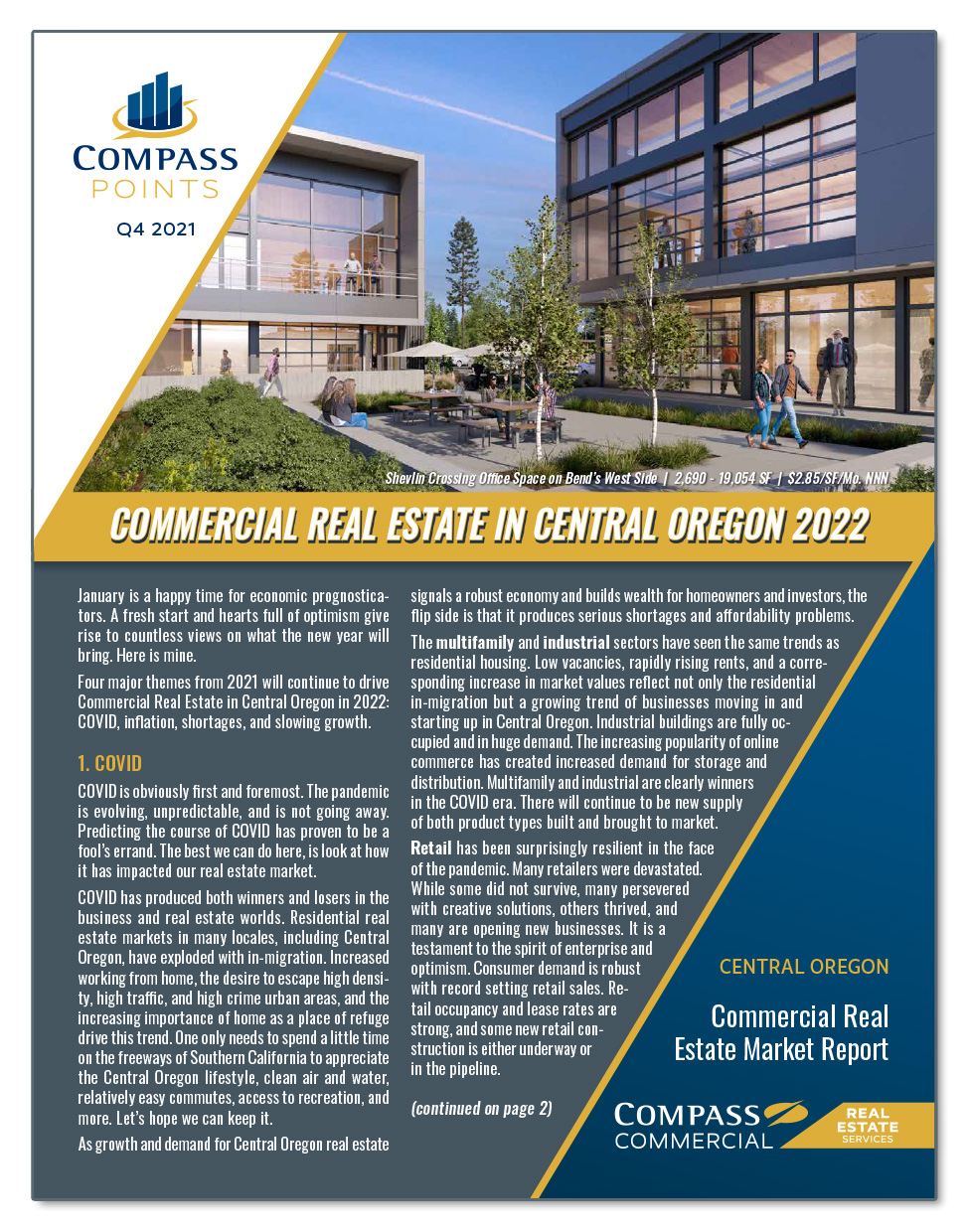

CONSTRUCTION: Brooks Resources and Taylor Development are moving forward with the development of Shevlin Crossing, a two-building Class A office project in NorthWest Crossing totaling approximately 45,054 SF. Construction of the first phase is slated to begin in April of this year. There are no speculative office developments currently under construction.

SALES: There were two notable sales this quarter. Pahlisch Homes purchased the Phoenix West Building, located in the Old Mill District at 384 SW Upper Terrace Drive, for $3,300,000 or $305/SF according to county records. This was an off-market sale. The 4,474 SF office building located at 452 NE Greenwood Avenue also sold for $1,320,000 or $295/SF.

Bend Retail Market

Written by partner and broker Russell Huntamer, CCIM

Compass Commercial surveyed over 4.58 million square feet of retail space across 261 buildings. During the quarter, 15,690 SF of positive absorption was recorded, resulting in the citywide vacancy rate dropping from 4.18% in Q3 to 3.78% in Q4. There is now 172,981 SF of available retail space for lease.

LEASING: Demand in the retail leasing market remained strong for Q4, with options becoming even more limited. The East Side submarket experienced the most activity this quarter, due to Pet Supplies Plus leasing 7,015 SF of the former Pier One space at The Forum Shopping Center. In the North 97 submarket, Black Steer Steakhouse and Saloon leased the former 6,772 SF Johnny Carino’s restaurant building and Crumbl Cookies leased 1,645 SF at Cascade Village Shopping Center.

RENTS: Asking rental rates for Bend retail space range between $1.50 and $3.33/SF/Mo. NNN* with the highest rates associated with

new construction.

CONSTRUCTION: Three construction projects are in the planning or permitting phase. Pioneer Marketplace at 1474 NW Wall Street is designed for 6,000 SF of retail space, with 1,500 SF preleased to Urban Waxx. The former Sonic site at 61165 S Hwy 97, a 4,793 SF retail and restaurant building is over 50% preleased and expected to begin construction in Q1. Reed South, an approximately 30,000 SF retail site located on the corner of Reed Market Road and 27th Street, has already began construction with leases pending.

SALES: There were three notable retail sales this quarter. Starbucks-anchored 1203 NE 3rd Street was purchased for $6,000,000 or $852/SF. The former Kebaba building at 1004 NW Newport Avenue sold for $1,120,000 or $969/SF and 431 NW Franklin Avenue, a mixed-use retail/residential building was purchased for $2,350,000 or $311/SF.

Bend Industrial Market

Written by partner and broker Graham Dent

Compass Commercial surveyed 320 industrial buildings in Bend, totaling 4.61 million square feet. At the end of Q4 the vacancy rate stood at 1.48%, down from 1.60% in Q3 due to 5,881 SF of net absorption during the quarter. Overall, the Bend industrial market absorbed a total of 89,392 SF in 2021 leaving just 68,058 SF available in the market.

LEASING: Demand for industrial space remained extremely high during the quarter. The number of lease transactions were limited only by the lack of available space. Many tenants are moving their industrial requirements to Redmond or having to seriously consider Redmond as an alternative due to tightened supply and rising costs in Bend.

RENTS: Average asking rates on Bend industrial space are between $0.95 and $1.25/SF/Mo. NNN*. Although the high end of these rates has generally been for new construction or highly improved industrial space, we are beginning to see second-generation industrial space command $1.00+/SF. The rise in rental rates is directly attributed to ever-increasing cost of construction and tightened land supply making development challenging.

CONSTRUCTION: There is one speculative industrial project under construction in the Northeast submarket at 63035 Lower Meadow Drive, totaling 11,840 SF, of which only 7,104 SF is available.

SALES: There were a handful of notable industrial building sales during the quarter. One property, located at 1105 SE Centennial Street, sold to an owner/user for $1,950,000 or $201/SF. Another property located at 2185 NE 2nd Street sold to an investor for $1,700,000 or $152/SF. A property at 20676 Carmen Loop sold for $4,000,000 or $155/SF. A small building located at 61523 American Loop with excess land sold to an owner/user for $1,100,000 or $326/SF, an indicator of where owner/user pricing is for small, well-located and functional properties.

Redmond Industrial Market

Written by partner and broker Pat Kesgard, CCIM

88 buildings totaling 1.66 million square feet were surveyed in the third quarter of 2021. In this quarter, the Redmond industrial market recorded positive net absorption of 3,250 SF. The majority of this absorption was at 4620 SW 23rd Street. The vacancy rate decreased as a result from 2.19% in Q3 to 2.00% in Q4. There is now 33,224 SF of industrial space available for lease. The 33,224 SF vacancy is in one building, and there are leases out for signature as of this report. This means there is virtually NO VACANCY in the Redmond industrial market.

LEASING: Activity in the Redmond industrial market continues to increase. As reflected in the nominal amount of vacancy, demand is growing.

RENTS: Average asking lease rates in the Redmond industrial market are between $0.85 and $1.10/SF/Mo. NNN*.

CONSTRUCTION: There is currently 90,000 to 100,000 SF of industrial space in the pipeline for 2022. Two industrial buildings at 2505 SE 1st Street totaling 58,568 SF are projected to be complete in Spring of 2022. Another 40,000 SF industrial building located at 2502 SE 1st Street is also slated to break ground at the end of 2022.

Positive Absorption = Space Leased | Negative Absorption = Space Vacated

*Data sourced from CoStar

Compass Points is Central Oregon’s primary commercial real estate newsletter. Compass Commercial Real Estate Services offers comprehensive surveys of office, retail and industrial properties in Bend and Redmond, Oregon. The report provides a detailed look at quarterly vacancy and absorption data in these markets along with leasing and sales activity, rental rates, construction projects and more.

To view the complete report with vacancy and absorption graphs, notable transactions and imagery, sign up to receive our quarterly publication at https://www.compasscommercial.com/POINTS or call (541) 383-2444.